|

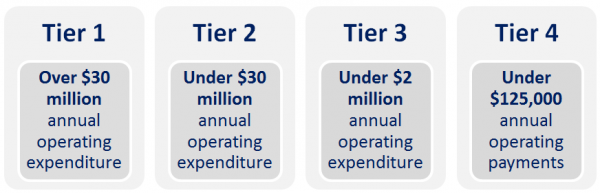

As from the 2016 financial year, charities are required to prepare their annual financial statements based on new reporting standards. In the XRB Standard A1, charities are referred to as Public Benefit Entities (PBE's). The fist thing to consider is if the entity (trust, company, society) is a Public Benefit Entity (not-for-profit) or if it is a for-profit entity. An op shop, for example, if it is a separate entity and the purpose is to provide funds to a trust that owns the entity and the trust is a not-for-profit, by virtue of the fact that the op shop's purpose is to make a profit and return this profit to a not-for-profit, means that it is in fact a for-profit entity. The degree of complexity is based on size ($ annual operating expenses) and whether or not the charity has public accountability (generally if it is listed or is a bank, credit union or insurance provider). There are four tiers. Tier 4 allows financial statements to be prepared on a cash basis. The Charities Commission is encouraging charities to commence using the new standards before they become obligatory. If you'd like to know more about how this will impact on your charity or interested in us assisting with preparation of your annual financial statements or even to set-up monthly management reporting for you, give me a call.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

A passion to see businesses flourish and charities enabled..

|

Search by typing & pressing enter

RSS Feed

RSS Feed